Ventures, equities, and new faces: 2026 Q3 letter

Re-examining our public-equities assumptions, a second venture in global health, welcoming Divya, understanding people, The Odyssey, and more…

Dear reader,

A lot has happened this quarter!

In this update, Peter shares how our venture-building arm is taking shape as the team’s growing independence lets him spend more time working directly with founders. Divya reflects on her first few weeks on the team, TJ and Zsolt take us behind the scenes of our equities process, Val writes about what she’s learned from spending time with founders and fund managers, and Justina reflects on what it means to really understand another person.

As always, thanks for reading. We’re grateful to have you along for the journey!

— All of us at Titanium Birch

Peter 👽

Venture building

I started Titanium Birch with a vision of compounding capital across a long time horizon — permanent capital with the freedom to allocate it however we think best. That means public equities, private-market funds, direct startup investments, and now, building companies ourselves. As the TB team has become increasingly independent at running the various sleeves of our portfolio, I’ve been able to shift more of my time towards working directly with founders from the earliest stages. That started with Fidaro (public beta now live — try it out!).

We’re now adding a second venture, in B2C global health. David Gilbert and Ed Bosher have joined as full-time founders, with Titanium Birch investing and providing operational support. We’re looking for another founder to round us out with deep marketing expertise. We can pay salaries, offer significant equity, and work collaboratively overseeing large teams of agents. Reach out if you’re interested, and please send referrals!

Growing the team

Divya just joined Titanium Birch to run talent acquisition for both Titanium Birch and the companies in our venture-building portfolio. An investor helping its portfolio companies with hiring has been one of the most practical examples of “operational value-add” in VC funds that we’ve seen. The team at Gutter Capital, for example, includes Head of Talent Richard Hughes, who coaches their founders on becoming great headhunters. Seeing that work well with Gutter was one of several motivations for bringing Divya on board. She was one of the driving forces behind ExpressVPN’s successful hiring, and I’m super happy to be working with her again.

Much hiring is coming soon. To find out about opportunities, make sure to follow us on LinkedIn.

Divya 🏹

Hey, folks! It’s the end of week 3 in my role at Titanium Birch, and I am extremely happy to be here!

It’s early days, and there are a lot of terms and concepts floating around that are still a little foreign to me, but that’s the learning curve I signed up for, so I’m very happy to be diving right in.

Having worked with Peter and TJ closely before, I had some expectations of what it might be like to team up again, and so far, I’m happy to say that everyone is exactly as supportive, friendly, and warm as I remember them to be.

I will be working hard to ramp up our hiring efforts, conceptualize some fun brand-building initiatives with Justina, who leads our branding, and strive to make this an even more fun place to work. Stay tuned! 🙂

P.S. We’re hiring!

TJ 🤖

Re-underwriting our equities portfolio

We spent a good chunk of 2025 making our allocations toward a globally diversified factor-tilted portfolio that accounted for what we felt were sources of long-term excess returns and discounted what we felt detracted from said returns.

Any deviations we made from the market portfolio were underpinned by certain assumptions about markets and the world. Our goal over the past few weeks was not to change this allocation, but to allow ourselves to falsify those assumptions with data. We think going through this process on a regular basis allows us to more systematically incorporate changes in the world without veering too much into active management.

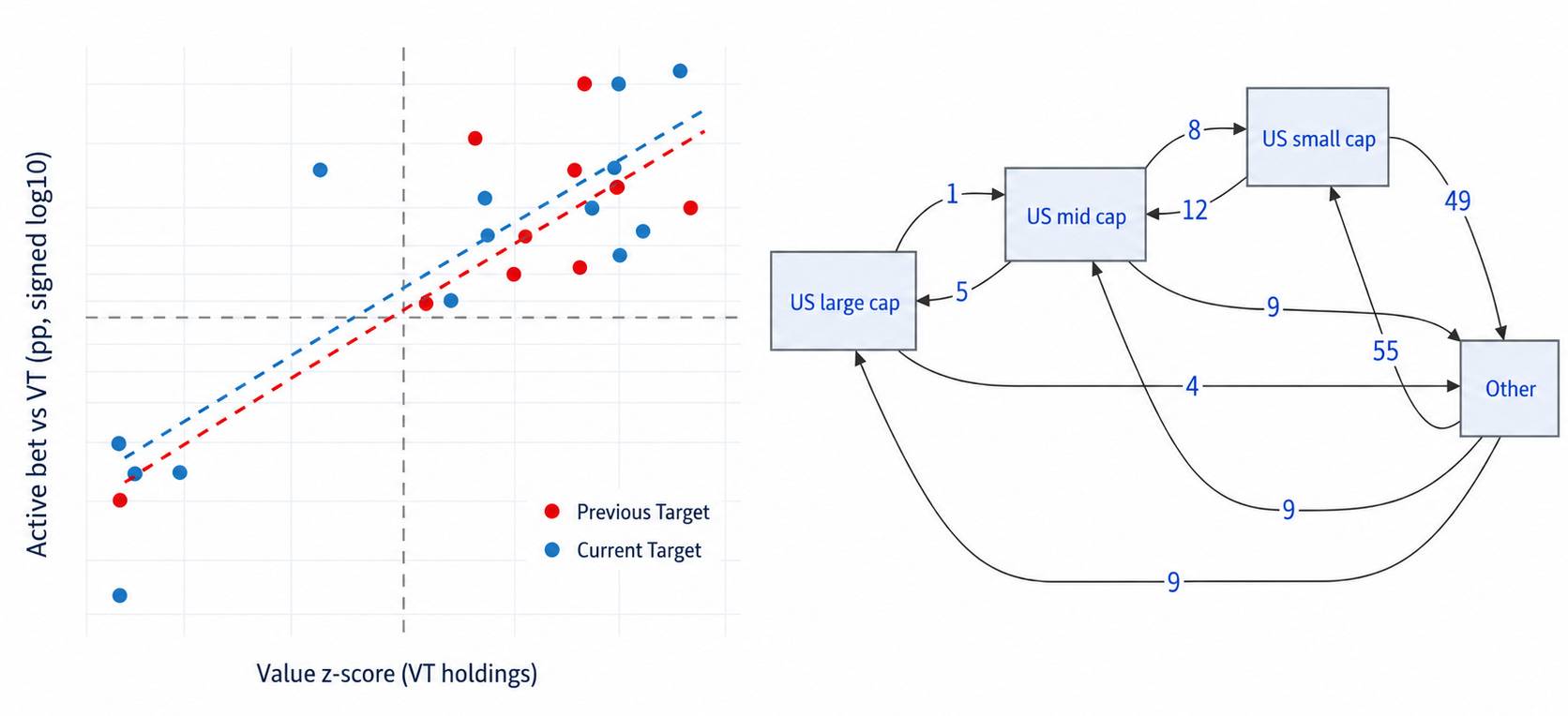

These are some (slightly anonymized) charts Zsolt and I produced during the analysis.

On the left: We were looking at our portfolio sub-sleeves and ensuring that our tilts continue to drive towards value despite market changes.

On the right: We were getting comfortable with index entrants and exits from US equity sleeves.

What’s next

We’re continuing to improve the foundations for our public equities strategy — reducing operational risks and getting into a healthy investment cadence — while looking to incorporate more information into our systematic investment process. It’s only the beginning, and we’re looking to hire an engineer to help accelerate our progress.

Zsolt 🌶️

Finding a new home for LedgerPigeon 🪺

Our accounting tool, LedgerPigeon, was originally built on AWS Athena, while most of our other components are already MotherDuck-native. This quarter, we decided it was time for LedgerPigeon to join the flock. Besides the performance improvements, bringing everything onto the same platform simplifies our workflows and makes it easier for our agents to query accounting data.

This has been the smoothest migration we’ve done so far. A big part of that came from reducing the manual effort to just the genuinely tricky edge cases — our agents took care of the rest.

What’s next

With TJ leading the effort, we now have a solid framework for making cash-deployment decisions. Our next focus is improving our desired exposure calculations, allowing us to execute trades more efficiently while steadily moving the portfolio toward our long-term target allocations.

Val 🌚

Time flies! This month marks my first year at Titanium Birch. We also welcomed our newest team member, Divya, and had a team-bonding event (a sound bath session!). I’m grateful to be part of the team and look forward to the year ahead.

We’re continuing to build out our VC program. After many GP meetings, I’ve found the most useful conversations aren’t the polished ones, but the candid discussions about how GPs make decisions: what concerns them, how they weigh risk, what gives them conviction, and what they learn from investments that haven’t worked out. Our goal is to understand not just a manager’s track record, but the quality of the thinking that produced it. Resume deep dives have been a critical component of this assessment.

We also attended several events organized by investors in the region. Spending time with founders and hearing the stories behind their companies reinforced just how difficult and uncertain the journey of building a company really is.

Justina 🐯

In June, I spent a few weeks in Toronto, New York, and San Francisco, getting to know folks in the North American VC community and seeing friends I hadn’t seen in almost a decade. It’s funny how, despite everything that’s changed over the last ten years, we’re all still recognizably ourselves. This question — what makes a person them? — is haunting me.

I’ve just started reading Daniel Mendelsohn’s delightfully readable translation of The Odyssey. Story time: in college, I signed up for an introductory comparative literature class. I don’t know what compelled me; I hated English class in high school, but I told myself to keep an open mind. Sitting in that tiny lecture hall, listening to my professor talk about The Odyssey, I could feel my world cracking open. Suddenly literature wasn’t just stories. It was a way of understanding people. Why do they do what they do? How do they see the world? How do we inhabit another person’s point of view?

I think most of my work at Titanium Birch is really an attempt to answer those same questions. My focus now is on building our venture portfolio through investing in VC funds and directly into startups. Whether we’re speaking with a founder, a GP, or a potential hire, we’re ultimately asking the same thing: Who is this person?

Part of our hiring and investment process involves a Topgrading-derived resume deep dive interview, where we ask someone to walk us through the story of their life and their career. It’s one of my favorite parts of the job. It doesn’t feel all that different from reading literature and trying to understand a character. What drives this person? What do they want most in the world? What are they willing to sacrifice to get it?

If understanding people is one of our core competencies as investors, we should also cultivate an environment where people feel safe telling each other what they really think. We built a custom prompt in Granola (our AI notetaker) to assess the level of psychological safety in our internal meetings. It flags behaviors that may undermine psychological safety (like interrupting, failing to invite dissent, or letting disagreement go unexplored) and offers actionable suggestions for improvement. After all, if we hope to accurately understand founders and GPs, we should first strive to accurately read our own room. The goal is to create better conditions for candor so we can improve our decision-making.

Who we’re hoping to hear from 📬

Software engineers. We’re hiring! If you love working at the intersection of code and capital (or know somebody who does), check out the job posting.

Founders. If you’re in Singapore or Hong Kong building something globally relevant, we’d love to connect. We write checks from $100k to $500k and work closely with founders who value high trust and direct communication. See if we’re a fit.

A GTM expert to join our B2C global health venture as a founder. Warm intros preferred if we’re not already connected.

If you found this post interesting, we’d be grateful if you could pass it along to a friend or leave a comment.

Until next time, thanks for tuning in!

Disclaimer: The content in this post should not be taken as investment advice.